November 17, 2021, 12:01 AM UTC

A world economy still struggling to shake off the Covid-19 crisis now faces an additional drag—a marked slowdown in China.

Based on Bloomberg Economics’ nowcasts, China’s gross domestic product is on pace to expand 5% in the fourth quarter, in line with the disappointing 4.9% pace of the previous three months and some way below the range of 6% to 7% recorded before the coronavirus.

The slump reflects the combined impact of a number of factors, first among them the weakness in real estate. The troubles of cash-strapped developer China Evergrande Group are emblematic of a sector that is overbuilt, overleveraged, and now—with sales slowing—struggling to pay its bills.

With property accounting for about 25% of China’s GDP, its woes exert a significant drag on the broader economy. Taken together with energy shortages, and recurring outbreaks of the virus, growth is now way below heady expectations of a continued ‘V’ shape rebound from last year’s contraction.

“China’s growth has slowed sharply and stimulus has yet to arrive” said Bloomberg economists Tom Orlik and Bjorn Van Roye. “The U.S. is already grappling with a five million shortfall in jobs, and the highest inflation in thirty years. The China slump risks adding to the list of problems.”

From U.S. retail sales to Chinese factory output, Bloomberg Economics’ nowcasts unite hundreds of data points to provide a high frequency read on the pace of growth and level of inflation across major economies ahead of the official data.

The accuracy of nowcast readings increases over the quarter as more data becomes available. The consensus forecast for China’s fourth quarter growth is currently 3.5%—even weaker than the nowcast reading. For the year as a whole, China is set to expand around 8%—reflecting strong first half growth from a low base in 2020.

For major advanced economies, the impact of the China slowdown has yet to be felt. The nowcasts show the U.S. on pace for a 4.6% annualized expansion in the fourth quarter. European powerhouse Germany is clocking a similar pace. And Japan, accelerating out of its lockdown slump, is also set for a strong quarter.

The picture for emerging markets is less impressive. India is slowing as initial recovery momentum fades.

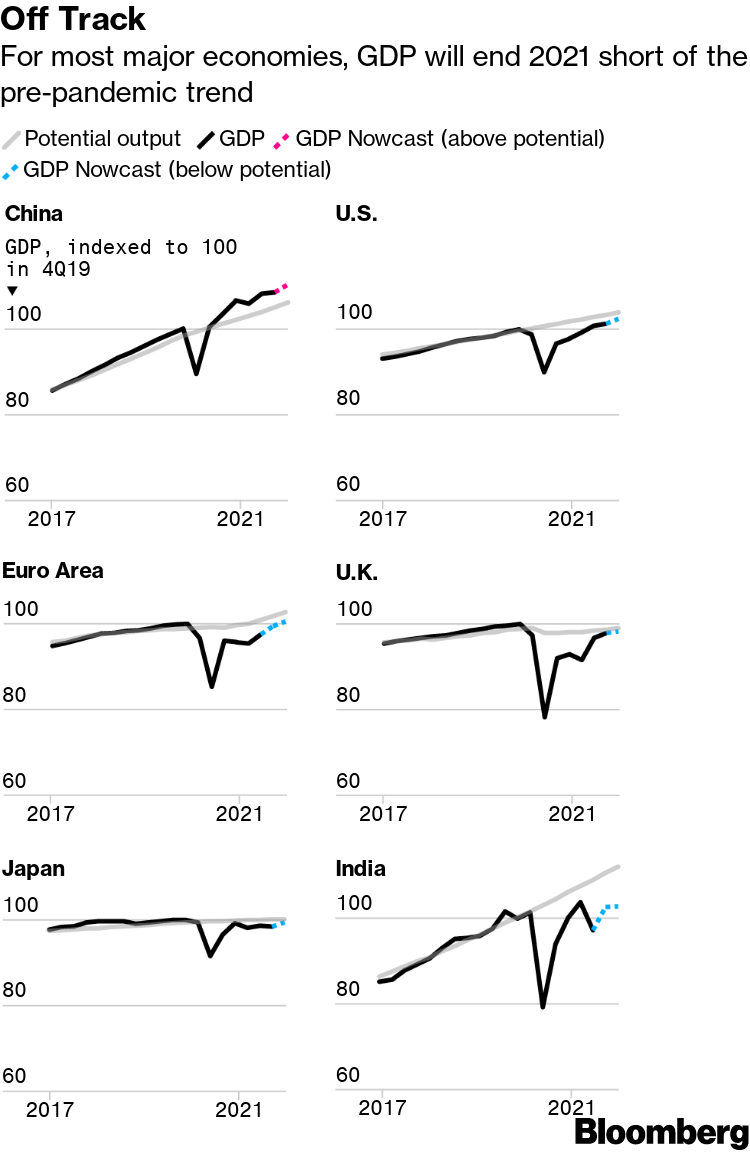

That mixed performance means most major economies will end 2021 with GDP still short of its pre-pandemic trajectory. If China’s growth fortunes don’t rapidly revive, the ripples from a slowdown in the world’s second biggest economy could knock recoveries further off track.

Off Track

For most major economies, GDP will end 2021 short of the pre-pandemic trend

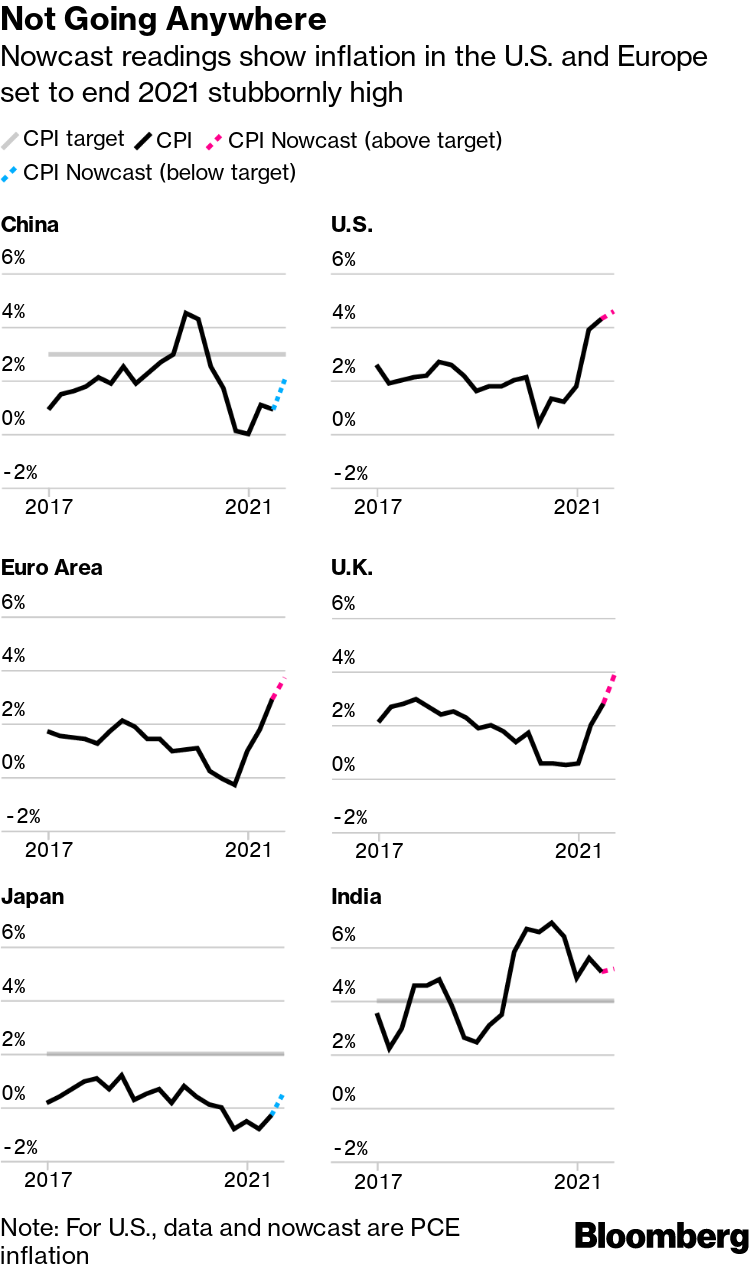

The China slowdown comes as the world economy grapples with another challenge—inflation that remains stubbornly high and may accelerate even faster. The nowcasts show U.S. inflation is set to end the year at 4.6%—more than double the Fed’s 2% target. Inflation in the euro area and U.K. is also running hot.

“Team Transitory”—the central bankers and economists who argued inflation would quickly fade—is in retreat. If there’s one silver lining from a China slowdown, though, it could be that weaker demand starts to take the heat out of prices. From oil to iron ore and soy beans, fears of weaker Chinese imports could trigger a drop in prices—which in turn would reduce sticker shock for consumers in the U.S. and Europe.

Not Going Anywhere

Nowcast readings show inflation in the U.S. and Europe set to end 2021 stubbornly high

Note: For U.S., data and nowcast are PCE inflation

For the world’s biggest central banks, 2021 has so far proved a humbling experience.

Predictions that inflation would ease proved wide of the mark—forcing an earlier than expected shift from pandemic stimulus toward a normalization of policy.

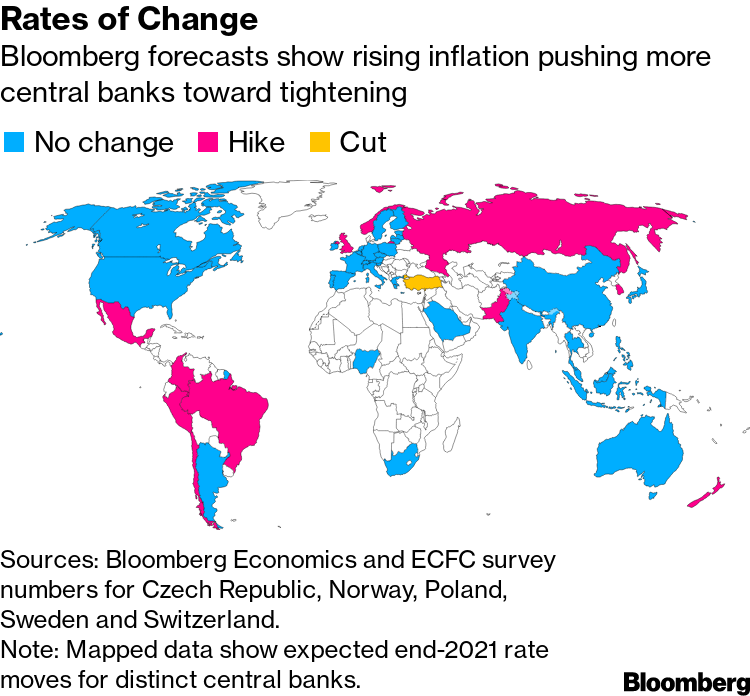

Rates of Change

Bloomberg forecasts show rising inflation pushing more central banks toward tightening

Note: Mapped data show expected end-2021 rate moves for distinct central banks. Sources: Bloomberg Economics and ECFC survey numbers for Czech Republic, Norway, Poland, Sweden and Switzerland.

The Bank of England missed market expectations for a first interest rate hike in November, but a move in the months ahead now appears all but inevitable. The Federal Reserve kicked off its taper of asset purchases at a rapid pace, opening a path to potential liftoff in rates in the second half of 2022.

The slowdown in China adds an important new variable. The People’s Bank of China has so far been slow to ride to the rescue, but if weakness is sustained Governor Yi Gang will almost certainly be forced to respond. Bloomberg economist Chang Shu expects a cut in the reserve requirement ratio—freeing more funds for banks to lend—before the end of this year.

For the rest of the world, China could bring another twist to the central bank drama. In 2015, the global risk-off moment triggered by the collapse in China’s stock market delayed the start of the Fed’s tightening cycle. The same thing could happen again.

More On Bloomberg